Revisiting the Privatization Debates of the 1990s: Part I

The Western origins of the Russian privatization debacle

“The Russians who blame Western advice for destroying their economy are not entirely wrong.” (Black et al. 2000)

“If McMillan is right that shock therapy was the problem, then the economics profession must accept some of the blame. Our profession lent some of its best and brightest to the transition effort, such as my former colleague Jeffrey Sachs. Most of these advisors pushed Russia to embrace a rapid transition to capitalism, If this was a mistake, as McMillan suggests, its enormity makes it one of the greatest blunders in world history.” (Mankiw 2003)

Historical Introduction

More than a quarter century has passed since the privatization debates raged in the international financial institutions (IFIs) and in academia concerning Russia and the other transition economies. There has been plenty of time for reflection and evaluation of these debates. Have the western advisory institutions learned any significant lessons from the Russian debacle, or have they essentially adopted the Sachs-Summers-Shleifer[1] strategy of quietly closing an embarrassing chapter in their history and moving their attention (and hopefully the public spotlight) on to the breathless pursuit of more immediate and pressing concerns? This note addresses two questions: the overall institutional change strategy and the arguments against and the alternatives to voucher privatization.[2]

There was a rough consensus view of privatization among post-socialist reformers and their western advisors. The stylized story goes something like this.

Privatize quickly and irreversibly to prevent a comeback of the nomenklatura. The quickest and most politically popular technique is mass voucher privatization.[3] However without intermediaries, this would spread the ownership too wide and would thus create the problem of “corporate governance.” Therefore, voucher privatization needs to be augmented by voucher investment funds to provide the necessary corporate governance for the restructuring of the privatized enterprises.

The first through-going voucher privatization in the post-socialist transition period of the early 1990’s was carried out in the Czech Republic.

By 1996 Prime Minister Klaus could state that the transition was more or less complete and henceforth the Czech Republic should be viewed as an ordinary European country undergoing ordinary political and economic problems. He characterized the voucher privatization program as ‘‘rapid and efficient.’’ Most observers and most World Bank staff working on the real sector in transition agreed. (Nellis 2007, 98)

The World Bank was far from alone in this; most other donors, including the EBRD, the EU, USAID, and several other bilaterals, endorsed, advanced, and supported this approach. (Ibid., 129)

A footnote then adds concerning the World Bank staff:

Not all, for example, David Ellerman (1998) had long expressed doubts as to the utility of the approach, and later wrote a strong critique of the approach. (Ibid., 129)

John Nellis was one of the key participants in the debates about privatization in the World Bank during the 1990’s. After he retired and after more than a decade of evidence accumulated, he reluctantly concluded:

The faith in the voucher approach was misplaced, or at least heavily over-emphasized. Stiglitz and others are correct to admonish the external advisory community; it – we – should have been searching earlier for ways to introduce concentrated owners; we should have paid more attention (earlier than we did) to prudential regulations in capital and financial markets and other institutional development matters. (Nellis 2007, 123)

The Stiglitz critique was forcefully given in his “Whither Reform?” paper delivered at the 1999 All Bank Conference on Development Economics (ABCDE) in Washington. As Stiglitz’s speech-writer at the time, I co-authored the paper but, in accordance with standard practice, was not listed as the co-author. The official Bank’s published version was somewhat edited, but the full version was later reprinted in Stiglitz (2001). The conclusions have held up quite well over the years.

If you want to support this work with employee ownership and workplace democracy, then please contribute to the:

Institute for Economic Democracy.

Institutional Change Strategies

History offers few “crucial experiments” but the contrast between the Russian and Chinese transitions is probably the best one could ask for to contrast an institutional shock therapy or blitzkrieg approach with an incremental, step-by-step, or staged approach to institutional change. As the Yeltsin reformers such as Anatoly Chubais did use rather “Bolshevik” methods to try to storm the ramparts during the few windows of opportunity, Stiglitz (2001) and Reddaway and Glinski (2001) have called this “market bolshevism.” A wise commentator has described these Bolshevik tactics well.

We have a fearful example in Russia today of the evils of insane and unnecessary haste. The sacrifices and losses of transition will be vastly greater if the pace is forced…. For it is of the nature of economic processes to be rooted in time. A rapid transition will involve so much pure destruction of wealth that the new state of affairs will be, at first, far worse than the old, and the grand experiment will be discredited.

These words are as true today as when they were written. And they were written by John Maynard Keynes (1933, 245) about the original Bolshevik transition, not today’s market Bolshevik transition in the opposite direction.

What was the alternative strategy? In this case, the incremental non-Bolshevik/Jacobin alternative has long found its sophisticated expression in the work of Albert Hirschman about incremental reform-mongering change driven more by endogenous pressures, bottlenecks, and linkages rather than by exogenous “carrots and sticks” embedded in IFI loan conditions.[4] The reform experience in China—which has never had an IMF program—represents something like this incremental approach in practice; crossing the river groping for the stepping stones rather than jumping over the chasm in one last “great leap forward.” As Deng Xiaoping put it in 1986.

We are engaged in an experiment. For us, it (reform) is something new, and we have to grope around to find our way. ...Our method is to sum up experience from time to time and correct mistakes whenever they are discovered, so that small errors will not grow into big ones. (see Harding 1987, 87)

When experiments had positive results, the idea was to then catalyze the process. As Chinese reformer Hu Qili put it at the same time:

We allow the little streams to flow. We simply watch in which direction the water flows. When the water flows in the right direction we build channels through which these streams can lead to the river of socialism.[5]

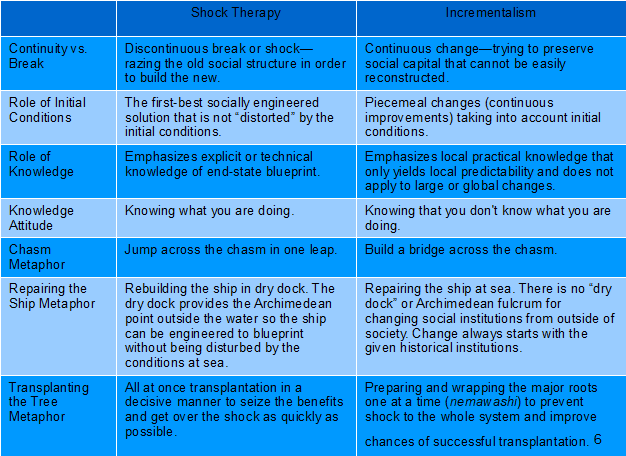

One of the important mis-formulations of the transition question was “Fast versus slow?” “Incremental” might be misleading if it is construed as “gradual” or “slow.” The Chinese reforms were neither gradual nor slow, and the Russians will not soon climb out of the chasm they failed to jump over in one leap. The point is to find and build step-by-step upon the reform efforts of the past (which requires taking into account past conditions) rather than trying to wipe the slate clean and legislate ideal institutions in one fell swoop. Murrell (1992) explored the connections between incrementalist strategies and conservative political philosophies. In Lau, Qian, and Roland (2000), the Chinese “two-track” system of reforms is analyzed where a second track, step, or stage is inaugurated and can then grow to eventually render the earlier stage obsolete. Black et al. (2000) use the word “staged” in much the same sense. In Joseph Stiglitz’s Whither Reform? (2001), the two “ideal types” were compared in a table as a “battle of metaphors.”

Table 1: “Battle of Metaphors”

Another part of the incremental approach, also evident in China, is the willingness to allow experiments in different parts of the country and then foster horizontal learning and the propagation of the successful experiments. This is an important part of the alternative to the Bolshevik/Jacobin approach of legislating the brave new world from the capital city to be applied uniformly across the country. The transition from socialism to a market economy had not happened before in history so the situation clearly called out for experimentation and pragmatism.[7] Instead the World Bank succumbed out of its own arrogance and “la rage de vouloir conclure” (the rage to conclude)[8] to the social-engineering Bolshevik/Jacobin mentality (complete with cold-warrior moral fervor to wipe the slate clean of past evils), with help from elite academic advisors, and supported Moscow legislation to apply the dreamed-up solutions across all of Russia.

Today, any passively voiced “mistakes-were-made” admissions are invariably accompanied by TINA pleadings—”There Is/was No Alternative.” But not only was it feasible for experiments to take place, they were taking place and were stopped in the market Bolshevik frenzy to legislate the brave new world during the window of opportunity. I will focus on the alternatives or “counterfactuals” available concerning privatization.

The Privatization Debates

After some initial limp resistance, the World Bank quickly succumbed to the public relations image[9] of the Czech voucher privatization as being “successful” and then promoted that model in other countries. In the rather standard model of voucher privatization, vouchers were distributed to all citizens, but it was expected that individuals would only invest the vouchers in mutual-fund-like voucher funds in return for shares in the funds. The funds would, in turn, use the vouchers to buy shares in the companies being privatized at state-run voucher auctions. But the voucher funds were run by fund management companies that could be completely owned by a few individuals or even by state-owned banks (e.g., in the Czech case). The voucher funds were supposed to be “controlling owners” who would supply “corporate governance” to the privatized companies. The companies were called “privatized” since their shares were predominantly held by the voucher funds which in turn were “owned” by millions of private citizens. But the funds were in fact controlled by the fund management firms which had negligible ownership interests[10] so the net effect was the “tunneling” of assets out various “back doors” to the benefit of the fund managers and their colleagues. Such was the scheme promoted by the IFI and academic experts in institutional design for “private property market economies.”

In a World Bank working paper later published in Challenge (Ellerman 2001) which, incidentally, circulated for several years around the Bank in samizdat form before Stiglitz arrived and allowed it to be brought out as a working paper as Ellerman (1998), I argued that the economic case for voucher privatization was remarkably superficial and that the basic rationale was political. Stiglitz (2001) and Stiglitz-Ellerman (2001) develop an additional argument as to why the voucher privatization programs such as the Russian scheme actually contributed to the debacle. This argument can be developed in different vocabularies.

The Argument in terms of Agency Chains

One approach is via the notion of agency chains.[11] Long agency chains are very difficult to police and maintain. Information economics emphasizes the “asymmetric information”[12] and monitoring failures in principal-agent relationships.[13] The longer the agency chain, the more the asymmetry and the greater the chances for opportunistic behavior. It took most of the 20th century to develop the array of watchdog institutions (e.g., accounting/auditing firms and the SEC) to police long agency chains in the West. A glance at runaway executive compensation in America, the ENRON-like scandals, and the collapse in 2008, show the continuing problems in making the system work. The market Bolsheviks tried to legislate and install institutions such as stock markets, watchdog agencies, and publicly traded companies as if all that could be done practically overnight.[14] Voucher privatization which threw most medium and large-sized companies into the stock market was an extreme “pathological” example of trying to legislate well-functioning long agency chains.[15]

Economists who are not blinded by ideology should know that market economies start with short, not long, agency chains—indeed, they start with the identity of principal and agent in owner-operated firms and farms. The decentralization that is part of building a market economy in transitional countries needs to similarly start with agency chains as short as possible, not as long as possible. In the Czech-style “model” of voucher privatization with investment funds generally preferred by the western advisors, the principal-agent ‘layers’ in the long agency chain were:

1. the millions of citizen-shareholders of voucher investment funds who were to control;

2. the boards of the funds which were supposed to control;

3. the fund management companies which were supposed to control;

4. the boards of their hundreds of portfolio companies which were supposed to control;

5. the managers of the portfolio companies who were supposed to control;

6. the middle managers and workers who were supposed to actually produce something that people were willing to buy.

Historians may find it hard to believe that the “experts” in the IFIs and in elite academia actually thought that such agency chains could be legislated and “installed,” and would then work reasonably well in economies after 70 years of communism.[16] And today, the comic-book version of the Russian debacle that is promulgated for public consumption is not the farcical nature of trying to legislate five-linked agency chains overnight. Instead the story is that “It didn’t work as planned” because of the rapacious managers and state officials who did not respect the legislated property rights. Thus, the fault lies not in the architects of the defenseless chicken coops but in the rapacious nature of the foxes.

The Argument in terms of de facto Property Rights

This analysis can also be approached using the notion of de facto property rights. Neoclassical economics tends to follow Ronald Coase and to emphasize the importance of establishing clear formal property rights (and then perhaps the market will do the rest). And the cartoon picture of the transition used by the IFIs and allied experts is one that hammers away on the importance of respecting “private property rights.” Never mind if the “clear-cut private property rights” are the ownership of junk-shares in voucher investment funds on the tail-end of many-layered agency chains. And never mind that in the U.S. economy (i.e., the experts’ implicit mental model) there has been a “separation of ownership and control” (Berle and Means 1932) for most of the 20th century so that the top managers who command the heights in this paradigm “private property market economy” do so on the basis of their organizational role (much like Communist Party officials) and de facto control of the board—not on the basis of their private property rights. Neoclassical cartoons tend to ignore such troublesome aspects of reality.[17]

Progress has been made on this question in Hernando de Soto’s books (1989; 2000). Although this was little noticed by the cheerleaders who wrote blurbs for his book jackets, including Ronald Coase, de Soto did not just argue for formal property rights but for the formalization of de facto property rights. That’s a horse of another color. After all, all the land occupied and farmed by peasants or occupied and used by slum dwellers already had formal owners; it was not part of some “commons.” The idea is that by using and improving these assets (formally but absentee owned by others), people have established certain de facto property rights which give them the capability to sow and reap. Any “reform” that would take away those de facto property rights (and the capabilities they represent) to assert absentee formal property rights would in fact be disempowering and anti-development. To promote market-driven development, the reforms should find out ways to formalize some socially acceptable approximation to those de facto rights so that the people then encounter the market and the private property system as something that empowers them—rather than the opposite.

Now transpose this argument over to the transition economies. In the decentralizing socialist reforms over the years and decades before 1990, the workers, managers, and local communities had developed a range of de facto property rights (or “use rights”) over their enterprises. Central planning never worked well and, as it got worse, forms of decentralization took hold in varying degrees across much of the socialist world. These reforms included the Yugoslav self-management system, the enterprise self-management councils of Hungarian “goulash” or reform communism, the Polish Solidarity-dominated self-management committees, and the Gorbachev perestroika reforms to increase enterprise self-accountability. One way or another, in often bizarre ways, people learned to do things in a twilight half-centralized and half-decentralized system. They developed de facto property rights that represented their capabilities to actually get a few things done and to squeak by.

When the spell was finally broken in 1989-90, the alternative to institutional shock therapy and market Bolshevism—the counterfactual—would have been to formalize the nearest approximation to the de facto property rights that would accepted as socially fair and thus continue the decentralizing thrust going “straight to the market” (e.g., through the lease buy-outs discussed later). If that alternative approach had been taken, then people would have encountered the market as something that would recognize and formalize the capabilities they had already developed and would allow them to do even better.

Instead the market Bolsheviks designed the so-called “market reforms” with the exact opposite purpose to deny the de facto property rights accumulated during the “communist past,” to righteously wipe the slate clean by re-nationalizing all companies of any size, and to start afresh with formal property rights deliberately unrelated to the previous “vestiges of communism.”[18] Sometimes these “ideal reforms” were compromised in getting legislation passed but, by and large, the “reforms” were successful in denying the de facto property rights acquired during the earlier decentralizing reforms. For instance, outside of a small elite, most Russians encountered the market not as something that strengthened their capabilities and empowered them to do more but as something that took away what they were capable of doing and left them in a position where the rational choice was to grab what they could in the face of a very uncertain and uncontrollable future.

These points are perhaps easier to understand when applied to dwellings. Here pragmatism tended to prevail over market Bolshevik ideology. People acquired various de facto property rights over their flats in the socialist countries (analogous to “squatters’ rights” in de Soto’s work). Since the distribution of housing also partially reflected the power relationships under communism, one might pursue the same logic to suggest that the slate should be wiped clean of the communist past and all apartments should be put on the market and auctioned off to the highest bidder. Just think of the efficiency gains by jump-starting the housing market! Instead most of the post-socialist countries figured out ways to arrive at formal rights that were the closest socially fair approximation to the de facto rights.

Moreover, this analysis and critique is not just “hindsight.” The following was written in 1992 and published (outside the World Bank) in 1993.

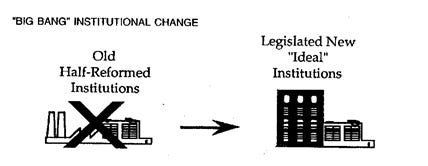

After the collapse of the socialist idea in the late 1980s and early 1990s, the question of institutional change strategies came to the forefront. Broadly speaking, two opposed strategies emerged. The Big Bang approach advocated just drawing a big X over the old half-reformed institutions and then legislating new “ideal” institutional forms.

Figure 1: Big Bank Institutional Change

The old de facto property rights embodied in the half-reformed institutions would not be recognized in any significant way, and the new de jure property rights would be legislated by the new “revolutionary” democratic government.

What is wrong with moving in one great leap to some desired ideal form? Nothing—if institutional change could actually take place in that manner. But it usually does not. People will resist and “drag their feet” in countless ways when their de facto property rights are canceled or trivialized. The imagined great leap breaks down in chaos. Instead of disappearing overnight in favor of the new ideal institutions, the de-legitimated old institutions break down in favor of a shadowy anarchy of ad hoc opportunistic forms. The Big Bang becomes a Big Bust.

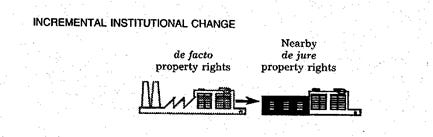

The alternative is a strategy of incremental institutional change. Instead of an imagined great leap forward over the chasm between socialism and capitalism, incentives would be devised to move people incrementally but irreversibly from the existing quasi-reformed institutions towards the “ideal” institutions. Instead of just negating the de facto property rights of managers and workers, they can arrive at a nearby set of legitimized de jure property rights by moving in the right direction.

Figure 2: Incremental Institutional Change

These two strategies are posed as opposites. No country would adopt a totally pure strategy, and one country might use both strategies in different parts of its reform program. For instance, the privatization-by-liquidation program in Poland is based on an incremental strategy while the Polish mass privatization plan originates from a Big Bang approach. The Czech voucher plan is a Big Bang strategy, while small business privatization in the Czech Republic (and in most other countries) is based on an incremental approach. Aside from the lease buyouts and other MEBOs, the Russian mass privatization program is a Big Bang program, while the Chinese reforms in agriculture and industry are the clearest example of a thoroughgoing incremental approach. (Ellerman 1993, 27-8)

References

Benziger, Vincent. 1996. “The Chinese Wisely Realized That They Did Not Know What They Were Doing.” Transition 7 (7-8 (July-August)): 6–7.

Berle, Adolf, and Gardiner Means. 1932. The Modern Corporation and Private Property. New York: MacMillan Company.

Black, Bernard, Reinier Kraakman, and Jonathan Hay. 1996. “Corporate Law from Scratch.” In Corporate Governance in Central Europe and Russia: Insiders and the State, edited by Roman Frydman, Cheryl W. Gray, and Andrzej Rapaczynski, 2:245–302. Budapest: Central European University Press.

Black, Bernard, Reinier Kraakman, and Anna Tarassova. 2000. “What Went Wrong With Russian Privatization.” Stanford Law Review 52: 1–84.

Blinder, Alan S. 1995. “Should the Formerly Socialist Economies Look East or West for a Model?” In Economics in a Changing World: Economic Growth and Capital and Labour Markets, edited by Jean-Paul Fitoussi, 5:3–24. New York: St. Martin’s Press.

Burke, Edmund. 1937. “Reflections on the French Revolution: In a Letter Intended to Have Been Sent to a Gentleman in Paris.” In The Harvard Classics: Edmund Burke, edited by Charles Eliot, 143–378. New York: Collier.

Byrd, William A, and Qingsong Lin. 1990. “China’s Rural Industry: An Introduction.” In China’s Rural Industry: Structure, Development, and Reform, edited by William A Byrd and Qingsong Lin, 3–18. Washington DC: Oxford University Press for the World Bank.

Coffee, John C. 1996. “Institutional Investors in Transitional Economies: Lessons from the Czech Experience.” In Corporate Governance in Central Europe and Russia: Volume 1 Banks, Funds, and Foreign Investors, edited by Roman Frydman, Cheryl W. Gray, and Andrzej Rapaczynski, 111–86. London: Central European University Press.

Dahrendorf, Ralf. 1990. Reflections on the Revolution in Europe: In a Letter Intended to Have Been Sent to a Gentleman in Warsaw. New York: Random House.

De Soto, Hernando. 1989. The Other Path: The Invisible Revolution in the Third World. New York: Harper & Row.

De Soto, Hernando. 2000. The Mystery of Capital. New York: Basic Books.

Ellerman, David. 1993. “Management and Employee Buy-Outs in Central and Eastern Europe: Introduction.” In Management and Employee Buy-Outs as a Technique of Privatization, edited by David Ellerman, 13–30. Ljubljana: Central and Eastern European Privatization Network.

Ellerman, David. 1998. “Voucher Privatization with Investment Funds: An Institutional Analysis.” Policy Research Paper No. 1924. Washington: World Bank.

Ellerman, David. 2001. “Lessons from East Europe’s Voucher Privatization.” Challenge: The Magazine of Economic Affairs 44 (4 July-August): 14–37.

Ellerman, David, Ales Vahcic, and Tea Petrin. 1991. “Privatization Controversies East and West.” Communist Economies and Economic Transformation 3 (3): 283–98.

Elster, Jon, C. Offe, and U. Preuss. 1998. Institutional Design in Post-Communist Societies: Rebuilding the Ship at Sea. Cambridge: Cambridge University Press.

Harding, Harry. 1987. China’s Second Revolution: Reform after Mao. Washington DC: Brookings Institution.

Hirschman, Albert O. 1973. Journeys Toward Progress. New York: Norton.

Keynes, John Maynard. 1933. “National Self-Sufficiency.” In The Collected Writings of John Maynard Keynes, edited by D. Moggeridge, 21:233–46. London: Cambridge University Press.

Kornai, Janos. 1990. The Road to a Free Economy. Shifting from a Socialist System: The Example of Hungary. New York: Norton.

Lau, Lawrence, Ying-Yi Qian, and Gerard Roland. 2000. “Reform without Losers: An Interpretation of China’s Dual-Track Approach to Transition.” Journal of Political Economy 108 (1): 120–43.

Mankiw, N. Gregory. 2003. “Review of: Reinventing the Bazaar (Book by John McMillan).” Journal of Economic Literature XLI (March): 256–57.

McClintock, David. 2006. “How Harvard Lost Russia.” Institutional Investor, January 24, 2006.

McMillan, John. 2002. Reinventing the Bazaar: A Natural History of Markets. New York: Norton.

Morita, Akio. 1986. Made in Japan. New York: E.P. Dutton.

Murrell, Peter. 1992. “Conservative Political Philosophy and the Strategy of Economic Transition.” Eastern European Politics and Societies 6 (1): 3–16.

Murrell, Peter. 1995. “The Transition According to Cambridge, Mass.” Journal of Economic Literature XXXIII (March): 164–78.

Nellis, John. 1999. Time to Rethink Privatization in Transition Economies? IFC Discussion Paper 38. Washington DC: International Finance Corporation.

Nellis, John. 2007. “Chapter 2: Leaps of Faith: Launching the Privatization Process in Transition.” In Privatization in Transition Economies: The Ongoing Story (Contemporary Studies in Economic and Financial Analysis, Volume 90), edited by Ira W. Lieberman and Daniel J. Kopf, 81–136. Bingley UK: Emerald Group Publishing. https://doi.org/10.1016/S1569-3759(07)00002-2.

Reddaway, Peter, and Dmitri Glinski. 2001. The Tragedy of Russia’s Reforms: Market Bolshevism Against Democracy. Washington DC: United States Institute of Peace Press.

Sachs, Jeffrey. 1993. Poland’s Jump to the Market Economy. Cambridge: MIT Press.

Scott, James C. 1998. Seeing Like a State: How Certain Schemes to Improve the Human Condition Have Failed. New Haven: Yale.

Stiglitz, Joseph E. 2001. “Whither Reform? —Ten Years of the Transition.” In Joseph Stiglitz and the World Bank: The Rebel Within, edited by Ha-Joon Chang, 127–71. London: Anthem Press.

Stiglitz, Joseph, and David Ellerman. 2001. “Not Poles Apart: ‘Whither Reform?’ And ‘Whence Reform?’” The Journal of Policy Reform 4 (4): 325–38. https://doi.org/10.1080/13841280108523424.

Tawney, Richard H. 1954. Religion and the Rise of Capitalism. New York: Mentor Books.

Tawney, Richard H. 1966. Land and Labor in China. Boston: Beacon Press.

Warsh, David. 1991. “In E. Europe, Major Differences in Privatization Yield to General Improvement.” Washington Post, May 15, 1991.

Warsh, David. 2018. Because They Could: The Harvard Russia Scandal (and NATO Enlargement) after Twenty-Five Years. CreateSpace Independent Publishing.

Weiss, Andrew, and Georgiy Nikitin. 1998. “Performance of Czech Companies by Ownership Structure.” Mimeo. Washington DC: World Bank.

Williams, Christopher. 1981. Origins of Form. New York: Architectural Book Publishing Co.

[1] The “Harvard wunderkinder,” Jeffrey Sachs, Larry Summers, and Andrei Shleifer, together with the Kremlin “Dream Team” (Summers’ memorable label) lead by Anatoly Chubais played a role in Yeltsin’s Russia roughly analogous to the “Chicago Boys” in Pinochet’s Chile. Peter Murrell has referred to their general strategy as “The Transition According to Cambridge, Mass.” (1995) but (as an M.I.T. alumnus) I must point out that the wunderkinder were all at Harvard.

[2] My main focus is on privatization prior to the Russian reformers’ “loans-for-shares” scheme—the latter which played a major role in creating today’s oligarchs and which was not publicly opposed by the IFIs. Many commentators seem to avoid learning difficult lessons from the earlier voucher privatization by focusing on the loan-for-shares scheme as the “Mother of all Debacles” instead of simply as “Dream Team: The Sequel.”

[3] While voucher privatization gives away for free the bulk of the assets on the asset side of the public balance sheet, one needs to consider the liabilities side of the balance sheet which includes:

· funding the daunting pension liabilities and health care needs of the aging population,

· meeting the interest and principal payments of the public and foreign debt,

· funding the social safety net and other economic dislocation costs,

· modernizing the education system to face the new challenges of a competitive market economy,

· paying to clean up after the environmental neglect of the past, and

· rebuilding the infrastructure needed for a modern economy. (see Ellerman, Vahcic, and Petrin 1991)

[4] See the “two basic approaches” in Hirschman (1973, 247-8) where he contrasts an ideological, fundamental, and root-and-branch approach to reform with an incremental, step-by-step, piecemeal, and adaptive approach.

[5] Quoted in: Harding (1987, 318). Thus do Chinese socialists instruct market Bolsheviks on the non-Bolshevik methods of institutional transformation. A related “pave the paths” metaphor is used by Christopher Williams (1981, 112). In a complex of new buildings, let grass grow between them, see where footpaths develop, and then pave the paths. While voicing Hayek’s ideas about the market as a spontaneous order, many market Bolsheviks (such as Václav Klaus) labored to totally stop spontaneous privatization instead of trying to find the closest socially acceptable channel so that those market forces might swell from a stream to a river (see Ellerman 1993).

[6] See Benziger (1996) on the Chinese “not knowing what they were doing,” Elster et al. (1998) for the use of Otto Neurath’s “rebuilding the ship at sea” metaphor in this context, and Morita (1986) on nemawashi.

[7] Deng Xiaoping’s pragmatism, “It is not important if the cat is black or white, but that it catches the mice,” was echoed by Ralf Dahrendorf’s 1990 call “to work by trial and error within institutions” (41; quoted in: Sachs 1993, 4). Dahrendorf’s book was a deliberate updating of Edmund Burke’s anti-Jacobin tract Reflections on the Revolution in France (1937, orig. 1790). Sachs argued against Dahrendorf’s pragmatism noting that: “If instead the philosophy were one of open experimentation, I doubt that the transformation would be possible at all, at least without costly and dangerous wrong turns.” (Sachs 1993, 5) To avoid “costly and dangerous wrong turns,” the then-Harvard wunderkinder promoted the scheme of mass privatization through voucher investment funds.

[8] See (Hirschman 1973, 238-40).

[9] Actually it was more than PR, at least in the usual sense. Some Bank economists churned out reams of accommodating econometric studies “scientifically” showing how “successful” the Czech privatization and restructuring was. Later, when Stiglitz had the econometrics redone outside the Bank, the results were negative or insignificant (see Weiss and Nikitin 1998). For a thoughtful rethinking of the Bank’s experience by the then-head of the Bank’s thematic group on privatization, see Nellis (1999 and 2007).

[10] The voucher funds were typically restricted by law to owning at most 20% or 30% of a portfolio company, and the annual payoff of the fund management companies was typically fixed at 2% of the value of the portfolio under management. Hence the “ownership interest” of the controlling fund management firms was on the order of 2% x 30% = 0.6% or six-tenths of one percent. This was not some “secret” design flaw discovered later; this was in the legislation of the voucher programs. Surely the experts, wunderkinder or not, could “do the math.” Yet the globe-trotting “institutional design experts” seemed surprised to later find in their voucher programs all across the transition economies that the fund management companies devised more efficient ways to “tunnel” funds (getting 100% rather than 0.6%) out various “back doors” of the firms. See Coffee (1996) for these and other typical details of voucher investment funds.

[11] An “agency chain” is a multi-linked chain of principal-agent relationships. For instance, in the large publicly traded U.S. companies, the theory is that the shareholders are the ultimate principals who “supervise and control” the board of directors as their agents (in theory through board elections but, in fact, dissidents tend to use exit—selling shares—rather than voice). The board, in turn, is supposed to select and supervise the top managers (rather than the other way around) in another link in the agency chain. Then the top managers supervise the middle managers and so forth eventually down to the workers on the office or shop floor.

[12] For instance, managers have much more relevant information about what they are doing and about the company than their “principals,” the board members and the shareholders.

[13] In 2001, Stiglitz received the Nobel Prize in Economics for his work in information economics.

[14] The superficiality of interpreting “passing laws” as institutional change (unfortunately, a common practice in the IFIs) was noted long ago by Richard Tawney after visiting China in 1930. “To lift the load of the past, China required, not merely new technical devices and new political forms, but new conceptions of law, administration and political obligations, and new standards of conduct in governments, administrators, and the society which produced them. The former could be, and were, borrowed. The latter had to be grown.” (Tawney 1966 (orig. 1932), 166)

[15] See “Corporate Law from Scratch” (Black, Kraakman, and Hay 1996) for a remarkable example of trying to etch first-best laws as if on a blank slate in Russia. Even more remarkable is that after much bitter experience with corporate governance in Russia, Black and Kraakman later reversed themselves (Black et al. 2000) and argued for a more pragmatic “staged” approach to legal and institutional development (see below on lease buyouts). The third author of “Corporate Law from Scratch”, Jonathan Hay, was a legal specialist from the Harvard Law School who worked with Shleifer in Russia on USAID contracts through Harvard. Shleifer and Hay were later indicted by the US Department of Justice for corrupt practices in that work and were convicted and fined on some counts and settled out of court on other counts. See McClintock (2006) and Warsh (2018).

[16] The attempts to use vouchers to kickstart “stock markets” in transition economies from the Czech Republic to Mongolia are best viewed as “cargo cult” reforms driven by the totemic or “religious” significance of “Wall Street” rather than by any real economic function (see Ellerman 1998, 2001). In this case, USAID presented a strong challenge to the World Bank/IMF to be “more Catholic than the Pope”—to be the true “Vatican” of the stock market cargo cult. Political appointees to ambassadorships in U.S. embassies in post-socialist countries had little patience with any incremental institution-building strategies; they wanted to see a “stock market” as soon as possible—even if it was little more than a Hollywood storefront or cargo-cult copy.

[17] James Scott’s book Seeing Like a State (1998) argues persuasively that states use simplified pictures of reality to administer their affairs but that these simplified pictures lead to disaster when they are the basis for large-scale social engineering schemes to change reality. Global development bureaucracies have even less contact with local realities than national governments and thus they tend to be even more driven by bureaucratic common-denominator stereotypes or cartoon models of reality.

[18] It is of some historical interest that (to my knowledge) no conservative or Austrian economist, political thinker, or social scientist publicly raised their voice to oppose the market Bolsheviks. This intellectual ‘prudence’ (a nice euphemism for cowardice) was probably due to their fear of being seen as soft on communism since the market Bolsheviks had framed the task as the great leap over the chasm between communism and capitalism. Otherwise conservative and Austrian thinkers can be very vocal in using their ‘principles’ to criticize any institutional change considered ‘socialistic.’ Critiques of the Bolshevik methods in the early 1990’s came from Dahrendorf (1990), Kornai (1990), Murrell (1992), Weitzman (1993), and the author (1993) none of whom would be considered as conservative or Austrian thinkers.

[19] “Shrink-wrapped ownership” is a metaphor denoting a structure where owners are those “stakeholders” who—independently of any formal ownership—have an “up close” functional relationship to the operations of a firm which would include the staff and major suppliers (including finance) or customers and perhaps local authorities but not, say, absentee buyers of second-hand shares. The idea is to match ownership to function with the firm rather than treat “ownership” as a tradable commodity that can be bought by otherwise unrelated parties. By “firm” I mean the de facto firm that meets every working day, not the formal legal entity that meets once a year. The strikingly successful Chinese TVEs (Weitzman and Xu 1994) function with a “shrink-wrapped” ownership/control structure even without western-style formal ownership—much to the bewilderment of the western experts.

[20] In the transition literature (e.g., Dabrowski et al. 2001), one sometimes finds the view that the industrial TVEs somehow sprung up de novo in the non-industrial countryside of China during the 80s and 90s. In fact, they started as the conversion and expansion of the commune (= township) and brigade (= village) enterprises left over from the earlier attempts to decentralize industry to the rural areas (see Byrd and Lin 1990).

[21] In a lease buyout, the enterprise staff—who developed de facto property rights in the decentralizing reforms—were allowed to proceed “straight to the market” by purchasing the company with seller-supplied credit on an installment or lease-purchase basis. As in U.S.-style leveraged buyouts and the Employee Stock Ownership Plans (ESOPs), the installment payments are made by the company (not the individuals) to the seller. The lease buyouts worked best as medium-sized (or smaller) firms. But the Soviet dinosaurs typically needed to be busted up into a related set of medium-sized firms, so lease-buyout “spin-offs” or “break-aways” could also be used to restructure and privatize large firms.